WORK

WAGES AND PERSONAL TAXES

In general terms, foreigners may be employed in Uruguay in all activities carried out throughout the national territory.

The immigration system in Uruguay provides different ways to enter the country including temporary residency, permanent residency, or non-residency. In order to work, foreigners must have either a temporary or permanent residency, granted by the Uruguayan National Immigration Office.

There are several mechanisms for setting wages:

-

Individual negotiation between employee and employer.

-

Bilateral negotiation with agreement between the company and the unions.

-

Tripartite negotiation in which the government participates along with workers and employers in setting the wage floor. Categories and readjustments are also determined through the Wages Councils (tripartite entities composed of representatives of the government, workers and employers).

Wage Levels

.jpg)

Compiled by Uruguay XXI based on surveys with specialized consulting firms and other companies in the same sector.

Personal Taxes

Individuals living in Uruguay are subject to Personal Income Tax. In addition, if they have assets located in Uruguay that exceed the non-taxable minimum (US$ 110,000, or twice that amount for family units), they must pay Wealth Tax.

Personal Income Tax (IRPF for its initials in Spanish)

Personal Income tax is a personal and direct tax levied on income earned by individuals living in Uruguay. Individuals are considered residents when they stay in Uruguay for over 183 days during a calendar year and establish their main activities or business, or have economic or vital interests in Uruguay.

Payment is made annually and is settled, as a general rule, on December 31st of each year. In any case, employed individuals must make monthly advances on this tax according to their different types of income (capital and/or work).

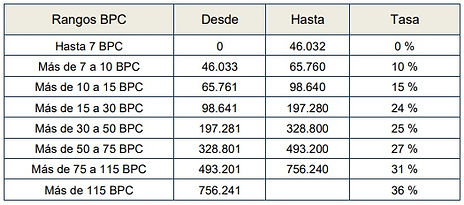

The rate is progressive, which means that the higher the income, the higher the tax:

1 BPC (Spanish acronym of Benefits and Taxes Basic Unit) = $ 4,519

Amounts expressed in Uruguayan pesos. See Uruguayan peso exchange rate here.

Other Taxes: Retirement Taxes, Health Insurance and Labor Reconversion Fund

Employees must also meet other requirements that ensure access by them and their family to the benefits they are entitled to (health, social security, accident insurance).

One of the requirements involves contributing a percentage of their monthly salary, which the employer will withhold therefrom and pay to the Social Security Bank (Spanish acronym: BPS). The personal contribution percentages withheld from their salary are as follows:

-

Retirement contribution: 15%

-

National Health Insurance: ranges between 3% and 8% depending on the income amount and the worker's family structure.

-

Labour Reconversion Fund: 0.125%

In certain sectors, it is very common for professionals to bill their fees to a company, for which it is necessary to establish:

-

A company providing professional services. In this case the professional must have their university degree approved in Uruguay and pay Personal Income Tax (IRPF)

-

A sole proprietorship, which will also pay Personal Income Tax (IRPF)

-

A Simplified Joint-Stock Company, which will pay Tax on Business Activities (Spanish acronym: IRAE). Technology service providers are exempt from this tax under the software Incentive regime.

Check the Social Security Bank's tax simulator here.